Iron Condors vs. Credit Spreads:

Which Structure Wins on Each Session Type?

The single most common question in 0DTE options: should I trade condors or spreads today? The answer isn't one or the other — it's which one matches today's session type. This is the definitive head-to-head comparison.

The Core Difference: Neutral vs. Directional

Before we compare performance, let's be precise about what these structures are and what they bet on:

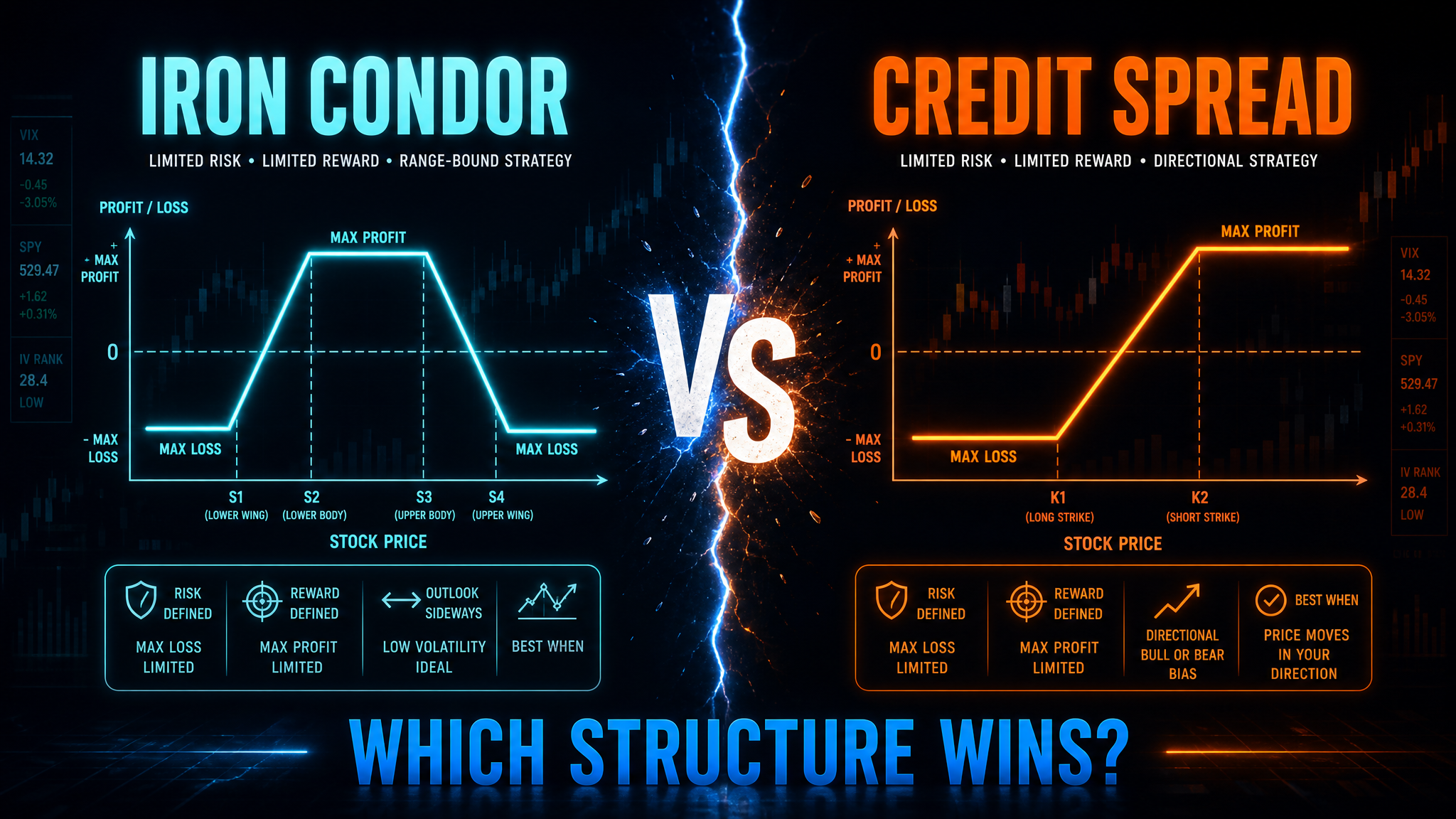

Iron Condor

- • Bet: Price stays in a range

- • Bias: Neutral / Non-directional

- • Legs: 4 (sell put spread + sell call spread)

- • Max Profit: Net premium collected

- • Reward:Risk: ~0.3:1 to 0.5:1

- • Best On: Balanced Day, Low Vol

Debit Spread

- • Bet: Price moves in one direction

- • Bias: Directional (bullish or bearish)

- • Legs: 2 (buy option + sell option)

- • Max Profit: Spread width minus debit paid

- • Reward:Risk: ~1.5:1 to 3:1

- • Best On: Trend Day, Expansion Day

The fundamental insight: an Iron Condor is a bet that the market stays still. A Debit Spread is a bet that the market moves. Neither is inherently better — but one is always more appropriate for the current market environment.

Anatomy of Each Structure (Side by Side)

Let's build both structures on SPX at 5800, so you can see exactly how the risk/reward compares:

SPX @ 5800 — 0DTE Structures Compared

| Metric | Iron Condor | Bull Put Debit Spread |

|---|---|---|

| Structure | Sell 5790/5785P + Sell 5810/5815C | Buy 5795P / Sell 5790P |

| Debit/Credit | Credit: $2.00 ($200) | Debit: $1.80 ($180) |

| Max Profit | $200 (if SPX stays 5790-5810) | $320 (if SPX < 5790) |

| Max Loss | $300 (width $5 minus $2 credit) | $180 (debit paid) |

| Reward:Risk | 0.67:1 | 1.78:1 |

| Breakevens | 5788 and 5812 | 5793.20 |

| Win Condition | SPX stays in a 24-pt range | SPX drops 7+ points |

| Management | 4 legs to monitor | 2 legs to monitor |

The numbers tell the story: Iron Condors offer higher probability, lower reward. Debit Spreads offer lower probability, higher reward. The question is: which probability profile matches today's market behavior?

The Session Type Matrix: Where Each Structure Wins

This is the core of the comparison. Not all days are the same, and the right structure on the wrong day is worse than no structure at all:

Mean-reverting price action keeps SPX within condor wings. High win rate.

Directional bets fail when price reverts. Low win rate.

1-2% directional moves breach one wing. Net loss despite winning side.

Strong momentum generates 2:1+ payoffs. Trend provides edge.

Wide range expansion demolishes condor wings. Potentially max loss.

Large moves create opportunities for wider target Debit Spreads.

Tight range favors premium selling, but low volatility means low premium.

Compressed ranges make directional bets difficult to profit from.

Sharp upward moves breach the call wing. One-sided loss.

Call Debit Spreads can capture the rally if timed correctly.

Violent whipsaws can breach both wings. Worst-case for condors.

Fade the sweep after completion with tight Debit Spread.

Iron Condors on Balanced Days: The Sweet Spot

Balanced Days are the natural habitat of the Iron Condor. Here's why the mechanics align perfectly:

- Mean reversion. Balanced Days exhibit strong mean-reverting behavior — price moves to the Initial Balance (IB) extreme, then reverses. This keeps SPX within a defined range, exactly what a condor needs.

- Theta harvesting. On Balanced Days, the range compresses as the session progresses. This accelerates theta decay on both sides of the condor, driving both wings toward zero faster.

- Positive GEX regime. Balanced Days typically coincide with positive Gamma Exposure (GEX), where dealer hedging activity suppresses volatility — acting as a natural tailwind for condors.

Balanced Day Condor Playbook

When: SPXXL classifies Balanced Day with 70+ confidence

Entry: After IB forms (10:00-10:30 AM ET). Sell wings 15-20 points from current price.

Width: $5-wide wings on both sides

Target: Close at 50% of max profit (don't get greedy)

Stop: If either wing breaches, close that side. Keep the winning side running.

Debit Spreads on Trend Days: The Momentum Play

Trend Days are where Debit Spreads shine and condors get destroyed. The mechanics are the opposite of Balanced Days:

- Persistent directional movement. Trend Days move 1-2% in one direction with minimal pullbacks. A $5-wide directional Debit Spread in the trend direction can go from $1.50 to $4.50 — a 3x return.

- Negative GEX amplification. Trend Days often coincide with negative GEX, where dealer hedging amplifies moves — they sell into weakness and buy into strength, feeding the trend.

- Gamma works for you. As SPX moves through your spread, gamma accelerates the value of your long leg faster than the short leg — the profit curve steepens as the trade works.

Trend Day Debit Spread Playbook

When: SPXXL classifies Trend Day with 70+ confidence

Entry: After first 15 minutes. Confirm trend direction. Buy Debit Spread ITM or ATM.

Direction: Bull Put Debit Spread on bearish trends. Bear Call Debit Spread on bullish trends.

Width: $5-wide spread at $1.50-$2.50 debit

Target: 80-100% of max profit (let trends run)

Stop: Close if debit loses 50% of value ($0.75-$1.25 remaining)

The Decision Flowchart

Use this framework every single trading day. It takes 60 seconds and eliminates the "which structure?" guessing game:

What is the SPXXL session classification?

Is the confidence score above 70?

Is today classified as Balanced Day?

Is today classified as Trend Day or Expansion Day?

Is today Volatility Compression, Liquidity Sweep, or Short Covering?

Risk Profiles Compared: What Can Go Wrong

Every structure has a failure mode. Understanding how each structure loses is more important than understanding how it wins:

Iron Condor Failure Modes

- Wing breach: SPX moves beyond one wing. Loss can exceed premium collected 2-3x.

- Gamma spike: Late-day volatility expansion can move SPX 20+ points in minutes, breaching wings that seemed safe.

- Slippage on 4 legs: Closing a losing condor under stress means 4 fills, each with potential slippage.

Debit Spread Failure Modes

- Wrong direction: Debit Spread in wrong direction = full debit lost. Max loss = 100% of investment.

- Range-bound market: On Balanced Days, directional Debit Spreads decay to zero as theta eats the premium.

- Late entry: Buying spreads after the trend is established means overpaying for premium. Early identification is key.

The critical difference in failure: When a Debit Spread fails, you lose exactly what you paid (defined). When an Iron Condor fails, you lose 2-3x what you collected (asymmetric). This is why Iron Condors must be traded on the right session type — the risk/reward only works when win rates are high.

The SPXXL Edge: Let the Classification Decide

The entire debate — condors vs. spreads — dissolves when you know what kind of day you're in. That's the entire point of session classification:

The Structure Selection Is Not a Strategy Decision.

It's a Classification Response.

Step 1

Classify

SPXXL identifies today's session type

Step 2

Select

Structure follows classification

Step 3

Execute

Mechanical rules, no hesitation

You don't choose the structure because you like condors or you're better at spreads. You choose the structure because the market told you what kind of day it is. Process over preference. Classification over conviction.

The right structure on the wrong day is the wrong structure.

Know the day first.

Start with a FREE trading week. 5 live sessions of session classification, confidence scores, and structure recommendations. See what kind of day it is before you decide.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. The strategy comparisons, win rates, and performance assessments in this article are based on historical session type analysis and are for educational purposes only. Past performance does not guarantee future results. SPXXL provides analytical tools and session classification — it does not provide financial advice or guaranteed outcomes. Always trade with capital you can afford to lose.