Why SPX Is a Different Animal

(And Powerful)

Most traders understand that SPX has tax advantages and cash settlement. But the real edge goes much deeper — into how the index actually moves, who moves it, and why it's structurally built for theta strategies.

S&P 500 Index = The Market Itself

SPX isn't a stock. It's the weighted average of the 500 largest companies in the United States. When you trade SPX, you're not trading one company's price action — you're trading macro behavior.

That means:

- SPX is the market — when SPX moves, almost everything moves

- No CEO tweets derailing your position

- No single-name earnings surprises wiping out your spread

You're trading the aggregate behavior of 500 companies. That diversification is baked into the instrument itself — and it's what makes SPX price action more statistically reliable than any single stock.

Cash Settlement (No Assignment Risk)

Unlike stock options, SPX options are cash-settled. No shares ever change hands. No early assignment. No pin risk stress at expiration.

This is enormous for structure traders:

- Your Condors and Verticals settle cleanly to cash

- No surprise 100-share positions appearing in your account

- No margin headaches from assignment on expiration day

For anyone running defined-risk strategies on 0DTE, cash settlement removes the single biggest operational risk.

The 60/40 Tax Edge Most Retail Misses

SPX options fall under Section 1256 Tax Treatment. Regardless of holding period — even if you held for 1 minute — gains are split:

60%

Long-term rate

40%

Short-term rate

TSLA trade

100% short-term tax on every gain

SPX trade

Blended lower rate — even on a 0DTE

Over a full year of active trading, the 60/40 treatment creates a massive compounding edge. Most retail traders leave this money on the table because they don't know SPX qualifies.

Multiple Expirations Including Daily 0DTE

SPX has expirations on:

- Monday, Wednesday, and Friday

- End-of-day settlements

- Daily 0DTE availability

This enables:

- Precision theta farming — choose exactly which day's decay curve you want

- Stacking trades multiple times per week without overlap

- Granular risk management — tighter windows mean smaller exposure periods

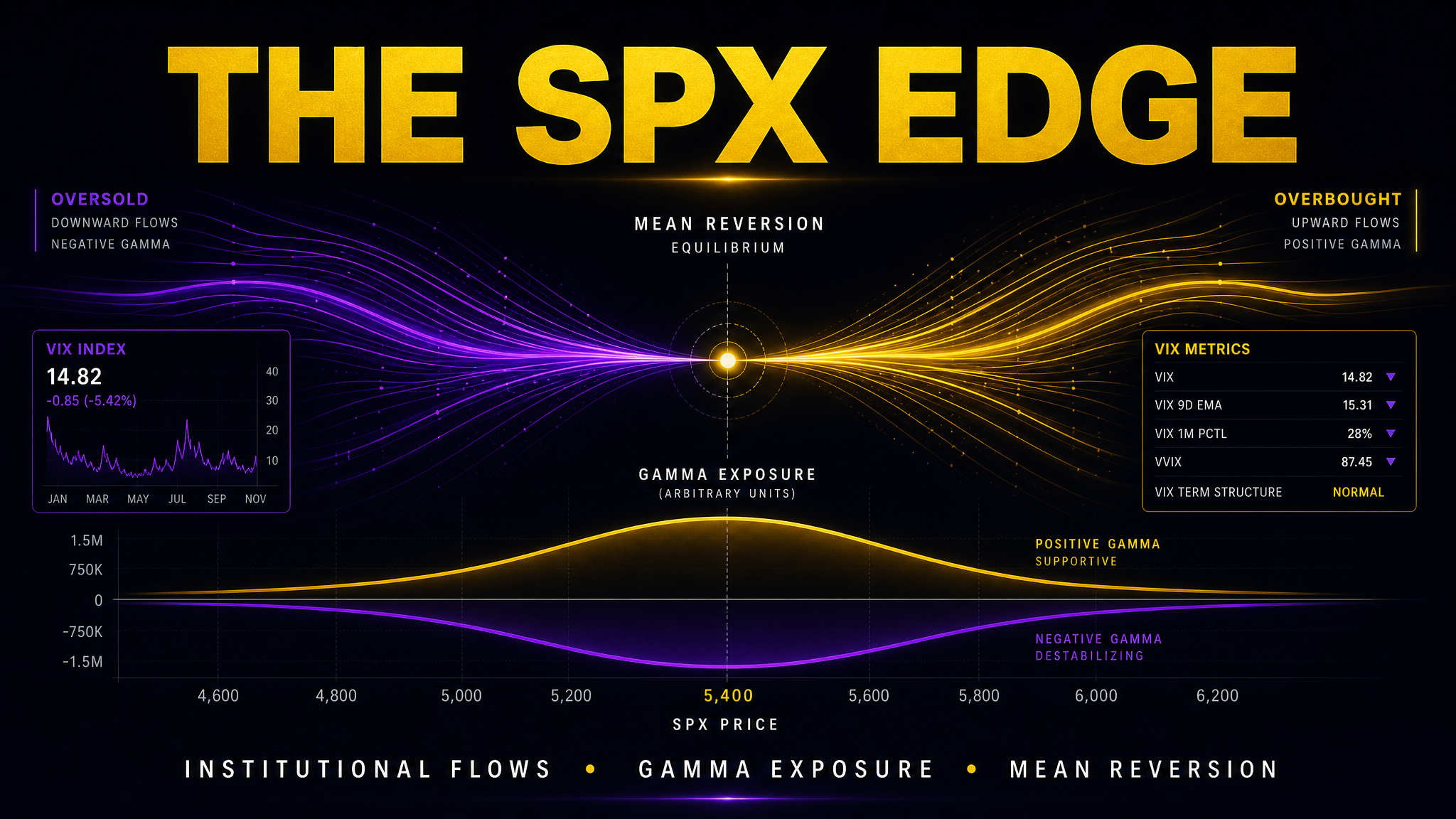

SPX Is a Mean-Reversion Machine

Unlike single stocks that can trend relentlessly on company-specific news, SPX tends to revert to the mean. Moves are more statistically “normal” — and there's a structural reason for this.

Because SPX is diversified across 500 companies, no single name can distort the index dramatically. One company's earnings miss gets diluted by 499 others.

This mean-reversion tendency is perfect for Debit Condors, Debit Butterflies, and range-bound structures. You're not betting against chaos — you're betting on statistical normality. And the index is structurally built to give you that.

Cleaner Expected Move Behavior

SPX respects implied volatility and expected move ranges much more reliably than single stocks.

When you calculate the expected move and place your strikes around it, the probability math actually holds up on SPX. On individual stocks? Not so much — because a single earnings report or analyst upgrade can blow the expected move completely.

Your core method — “place strikes around expected move” — works way better on SPX than on any single stock. The math is cleaner because the underlying is more statistically predictable.

No Overnight Gap Risk From Single Events

Single stocks are chaos magnets:

- Earnings = massive overnight gap

- CEO resignation = instant drop

- Analyst downgrade = surprise selloff

SPX only reacts to macro events — Fed decisions, CPI releases, jobs data. And here's the key:

Macro events are scheduled. You know when FOMC meets. You know when CPI drops. You can plan around them. Stock earnings? You're guessing which day some CEO decides to pre-announce.

Liquidity Is Elite

SPX options have:

- Extremely tight bid-ask spreads

- Massive daily volume across all strikes

- Deep institutional participation from market makers and hedge funds

What this means in practice:

- Easier fills — even on multi-leg strategies

- More accurate pricing — what you see is what you get

- Less slippage — tighter spreads = better execution

Built for Theta Strategies

SPX is basically a professional playground for time decay strategies. Here's why:

- Predictable IV behavior — implied volatility follows consistent patterns

- Smooth decay curve — theta burns evenly, especially on 0DTE

- Strong options market makers — tight quotes mean fair pricing for sellers

Your strategies — Condors, Verticals, Butterflies — thrive here because the underlying is stable enough to collect premium on, but volatile enough that the premium exists in the first place. That's the sweet spot.

The Hidden Truth: SPX Is Driven by Flows

Most people think “SPX moves because of news.” That's not the full story.

SPX is heavily influenced by institutional positioning:

Institutional Hedging

Pension funds, hedge funds, and market makers run massive hedging programs in SPX options. Their flows create structure in the market.

Dealer Positioning (Gamma)

When dealers are long gamma → market stays range-bound. When dealers are short gamma → market trends hard. This dynamic is the invisible hand behind most SPX intraday behavior.

Understanding who is positioned and how gives you a massive edge in selecting the right strategy for the day.

Gamma Exposure (GEX) = Secret Weapon

This is advanced, but powerful:

Positive Gamma

Dealers are long gamma

- Market pins and ranges

- PERFECT for Condors

Negative Gamma

Dealers are short gamma

- Big trending moves

- Dangerous for Condors

This explains why some weeks your strategy prints money and other weeks it gets crushed. It's not random — it's gamma positioning. When you can identify the dealer regime, you can choose the right structure before placing the trade.

Volatility Products Influence SPX

SPX is directly tied to VIX — the market's expectation of future volatility.

VIX Rising

Options get expensive

Premium expands

VIX Falling

Options decay faster

Theta accelerates

This directly impacts your entry pricing and your theta profits. Understanding the VIX regime tells you whether to be aggressive with premium selling or to tighten your wings.

Why Your Strategy Gets Better on SPX

Let's compare what matters for a theta-based 0DTE system:

Conclusion: Your theta farming system becomes dramatically more predictable when applied to SPX. Every factor that matters — from mean reversion to liquidity to tax — favors the index.

What Most People Miss

SPX is “safer”… until it's not.

When SPX Gets Dangerous

- Fed announcements — rates decision + press conference = maximum uncertainty

- CPI days — inflation data can whipsaw the index 50+ points in minutes

- Black swan events — geopolitical shocks, systemic failures, liquidity crises

When volatility expands, Condors can blow through both sides fast. The same mean-reversion tendency that normally helps you can reverse into a trending monster.

This is exactly why session classification matters. You need to know the regime before you place the trade — not after your Condor is already underwater.

The Real Edge (What You're Building)

When you combine:

Expected Move: Know the statistical range before placing strikes

Theta Decay: Harvest time decay on the most predictable underlying

Range Probability: Use mean-reversion and ADR levels to define boundaries

Session Classification: Identify the regime before committing capital

Gamma Awareness: Understand dealer positioning to know when to be aggressive

…on the most statistically stable underlying in the options market.

That's not gambling anymore. That's volatility trading with structure.