The Hidden Order Book Behind Your 0DTE Trades

How dealer gamma exposure, vanna sensitivity, and the “implied order book” drive every SPX session type — and why SPXXL’s classification engine is built on the same institutional framework that powers dealer hedging desks.

You're Trading Inside Someone Else's Hedge

Every time you trade a 0DTE SPX option, there is a dealer on the other side of that trade. And that dealer must hedge.

This isn't optional. It's a survival requirement. When you buy a put, the dealer is implicitly taking the inverse of your position. To neutralize the directional risk, they dynamically buy or sell the underlying index — a process called delta-hedging. The result? Every option trade you place creates a cascade of buy and sell orders in the S&P 500 itself.

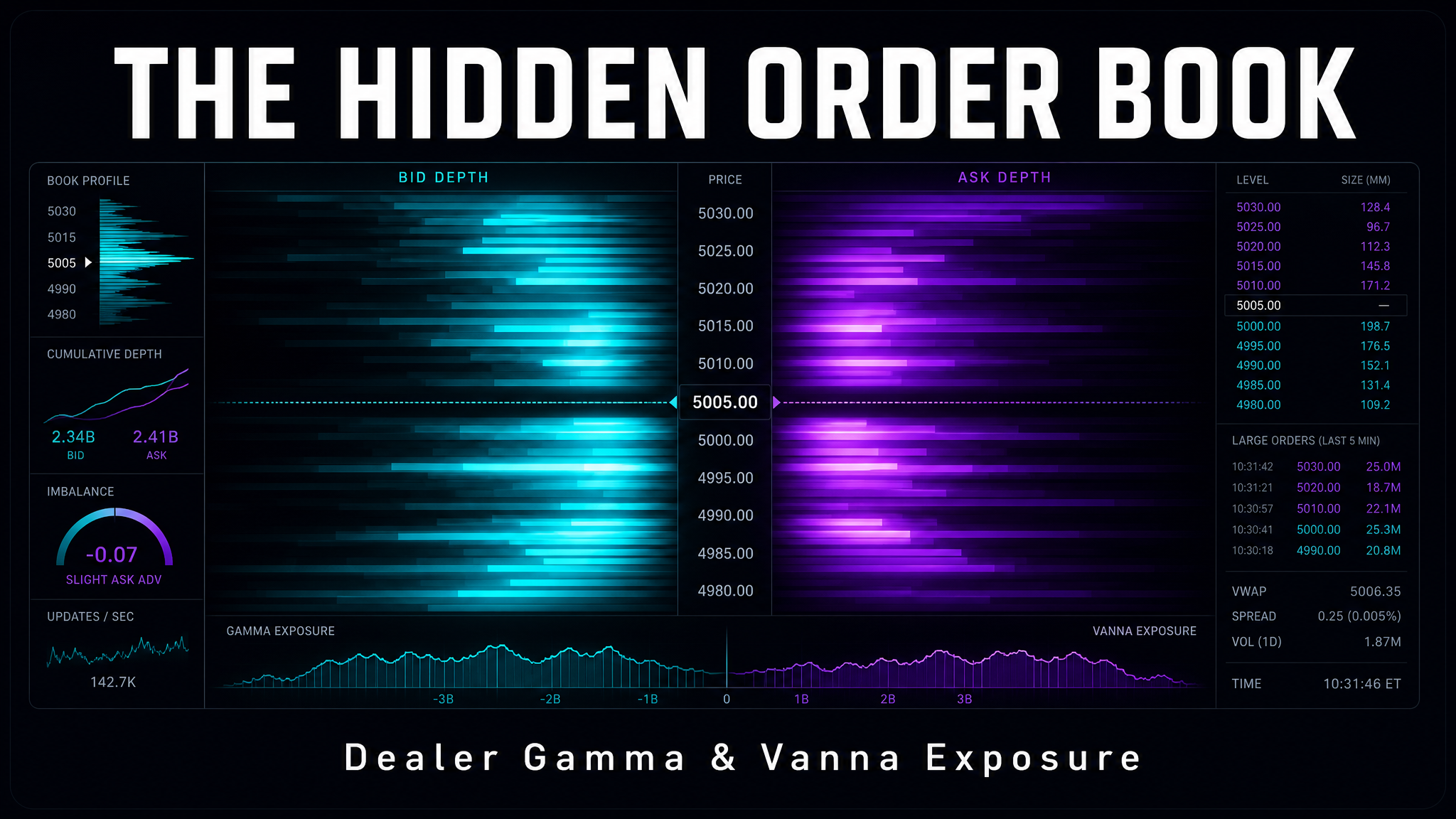

The real limit order book is invisible — fragmented across tens of dark pools, hundreds of order types, and limitless algorithmic routing systems. But options create a predictable, measurable shadow of it. That shadow is the implied order book.

This matters more now than ever. Since the PDT rule was eliminated on June 4, 2026, 0DTE volume has exploded. Retail 0DTE traders are now a meaningful force in this hedging ecosystem. Every Debit Condor, every Butterfly, every options trade you place — it all feeds into the same dealer hedging machinery that drives index liquidity.

SPX options are the largest, most transparent part of the broad market's order book. We can measure, by analyzing transaction data, where delta-hedges must occur. And from that, we can build a uniquely information-rich view of where liquidity is abundant — and where it's scarce.

Options Are Order Types, Not Instruments

Most traders think of options as a separate asset class from equities. But from the perspective of market structure, options are better understood as a complex order type — a way to take or supply liquidity in the underlying.

When you SELL an option

You're indirectly adding liquidity to the market. The dealer hedges by placing limit orders on both sides of the market — buying dips, selling rips. This stabilizes price.

When you BUY an option

You're effectively placing stop-loss orders above and below the market. The dealer must chase price in the direction it's moving — buying as it rises, selling as it falls. This destabilizes price.

The supply and demand picture of the S&P 500 is determined more by option positioning than by equity flows. That's a paradigm shift — and it's the reason SPXXL exists.

GEX: Why Some Days Trade in a 20-Point Box and Others Move 80+

Gamma Exposure (GEX) measures how much dealer hedging adds or removes liquidity based on changes in the underlying price. It's the answer to a question every 0DTE trader has asked: "Why is today so dead?"

GEX → Session Type Mapping

Dealer hedging compresses range. Every dip gets bought, every rally gets sold. Tight, two-sided auction — theta trader's paradise.

Enough liquidity for orderly price discovery, but not enough to contain a directional imbalance. One-way streets develop.

Dealer hedging withdraws. Normal ranges don't apply. Wide moves, stop-hunting, and volatility events dominate.

When SPXXL classifies a Volatility Compression session with high confidence, there's institutional mechanics behind it — not just pattern matching. The market's gamma exposure is physically resisting price movement in both directions.

GEX is very rarely negative. Even when it is, it's never historically been below $-200mm per SPX point. In the vast majority of cases, GEX shows us that SPX option dealers are providing a great deal of liquidity — sometimes over $1 billion per point. The proof is in the volatility: higher GEX corresponds to tighter daily ranges. This isn't the flaky kind of liquidity that an HFT market-maker provides — this is high-quality, guaranteed liquidity.

Vanna: Gamma's Evil Twin

If GEX is the stabilizing force, Vanna Exposure (VEX) is the destabilizing one. VEX measures dealers' delta sensitivity to changes in implied volatility — not price.

Here's the terrifying part: the most common SPX option flows (buying OTM puts, selling OTM calls) create a momentum effect via vanna that amplifies crashes. When IVs rise — usually because liquidity is already deteriorating — both of these positions force dealers to sell the index. More selling → lower prices → higher IV → more forced selling. It's a feedback loop.

The Crash Feedback Loop

The crash only ends when VIX is so high that it can only go lower. Then VEX flips — forcing dealers to buy just as aggressively as they sold. Cue insane bear-market rallies.

This maps directly to SPXXL's Liquidity Sweep session type. These events often occur at GEX zero-crossings where vanna dominates — the market "sweeps the floor" of stop-losses, absorbing liquidity before reversing. The large wicks on the chart are the tell-tale vanna signature.

Ironically, bought puts — despite being a liquidity-taking order type — end up actually adding a small amount of liquidity when things really fall apart (because their vanna flips). The only thing that causes sustained 20-30% crashes is when too many people sell puts, creating such enormous latent demand for liquidity that one spark triggers an unstoppable chain reaction.

The Map: Reading Conditional Liquidity for 0DTE Structure Selection

Knowing the current liquidity situation isn't enough. To make good decisions, you need to know about conditional liquidity. What happens to the order book if SPX falls 5%? What if VIX spikes 20 points? What if it drops 10?

GEX+ (GEX + VEX) is the full picture — total option-originated liquidity. It ranges from +$2 billion (extremely stabilizing) all the way down to -$500 million (crash territory). By mapping GEX+ across different price and volatility scenarios, you get a heat map of the implied order book — a "liquidity map" that shows exactly where dealer hedging provides support and where it doesn't.

Why This Matters for Structure Selection

GEX+ at +$1.5B

Debit Condor / Debit Butterfly territory. Dealer hedging creates a thick cushion on both sides. Range stays compressed — ideal for range-bound debit structures.

GEX+ at +$200M

Thin ice. Minimal dealer support. One directional push and the market moves fast — your Condor wings get tested.

When SPXXL recommends a Butterfly in a Balanced Day vs. a Call Spread in a Trend Day, it's sensing the same liquidity regime that institutional desks are modeling. The classification engine doesn't just see patterns — it reads the structural mechanics underneath them.

What This Means for Your Trading: 3 Rules from the Implied Order Book

Range is not random

The daily range of the S&P 500 is a direct function of measurable dealer positioning. When GEX is above $1 billion, average daily moves tighten to 0.20%. When VEX goes deeply negative, average daily moves expand to 6.00%. SPXXL's session classification captures exactly this — a Balanced Day with 80%+ confidence isn't a guess. It's reflecting quantifiable institutional mechanics.

Volatility is liquidity

When VIX is low, it's not "complacency" — it's abundant dealer-supplied liquidity. Options are the order book, and when enough options have been sold to create massive positive GEX, volatility is physically suppressed. When VIX spikes, it's not "fear" in some vague emotional sense — it's liquidity being withdrawn from the market through dealer hedging mechanics.

The transition is the edge

The most profitable 0DTE trades happen at session transitions — when the GEX regime shifts. A market that was in high-GEX Volatility Compression all morning and then breaks out doesn't just "go up" — it transitions from one liquidity regime to another. SPXXL's real-time classification and transition alerts are designed to catch exactly this moment.

How SPXXL Operationalizes This Framework

You don't need a $50 million data operation to trade with the implied order book. SPXXL's classification engine distills these institutional mechanics into actionable signals every 30 seconds:

- 6 session archetypes — each mapping to a specific GEX/VEX liquidity regime

- 7-dimension scoring engine — with a new Liquidity Score that proxies dealer gamma/vanna exposure using VIX, range compression, and VWAP adherence

- Real-time liquidity regime badge — showing whether the current environment is High, Normal, or Low liquidity at a glance

- Structure recommendations — calibrated to the current liquidity regime, not just pattern-matched to historical session types

- Session transition alerts — notifying you the moment the classification engine detects a regime shift, so you can adjust structures in real-time

SPXXL's classification engine is built on the same institutional framework that powers dealer hedging desks — gamma exposure, vanna sensitivity, and the implied order book. We translate these mechanics into real-time session types so you always know the liquidity regime before placing your 0DTE trade.