The Complete Guide to 0DTE Options Trading

Zero days to expiration options have exploded from a niche strategy to nearly 50% of all SPX options volume. This guide covers everything you need to know — from the mechanics that make them unique to the strategies, risks, and frameworks professional traders use to capture theta decay before the closing bell.

What Are 0DTE Options?

0DTE (zero days to expiration) options are contracts that expire on the same day they are traded. When you buy or sell a 0DTE option at market open, it will either be worth something or expire worthless by the 4:15 PM ET close.

This isn't a new instrument — it's a time frame. Any option becomes a 0DTE option on its expiration day. What changed is that the Cboe introduced daily expirations for SPX in 2022, meaning every trading day is now an expiration day.

The result: traders can now implement defined-risk, single-session strategies without overnight exposure — and the market responded. 0DTE contracts now account for over 50% of all SPX options volume on most trading days.

Why 0DTE Options Exploded in Popularity

There are five structural reasons behind the 0DTE explosion:

- No overnight risk. Your position is opened and closed within a single session. No earnings surprises, no geopolitical events while you sleep.

- Defined risk by default. Spreads and butterflies have maximum loss baked into the structure. You know your worst case before entry.

- Capital efficiency. SPX 0DTE Debit Spreads can be opened for a fraction of the capital required for multi-day positions, freeing up buying power.

- Rapid feedback loops. You get a result every single day. Win or lose, the cycle completes — and you refine your approach for tomorrow.

- Premium selling edge. Time decay accelerates exponentially as expiration approaches. Theta sellers harvest the fastest portion of the decay curve.

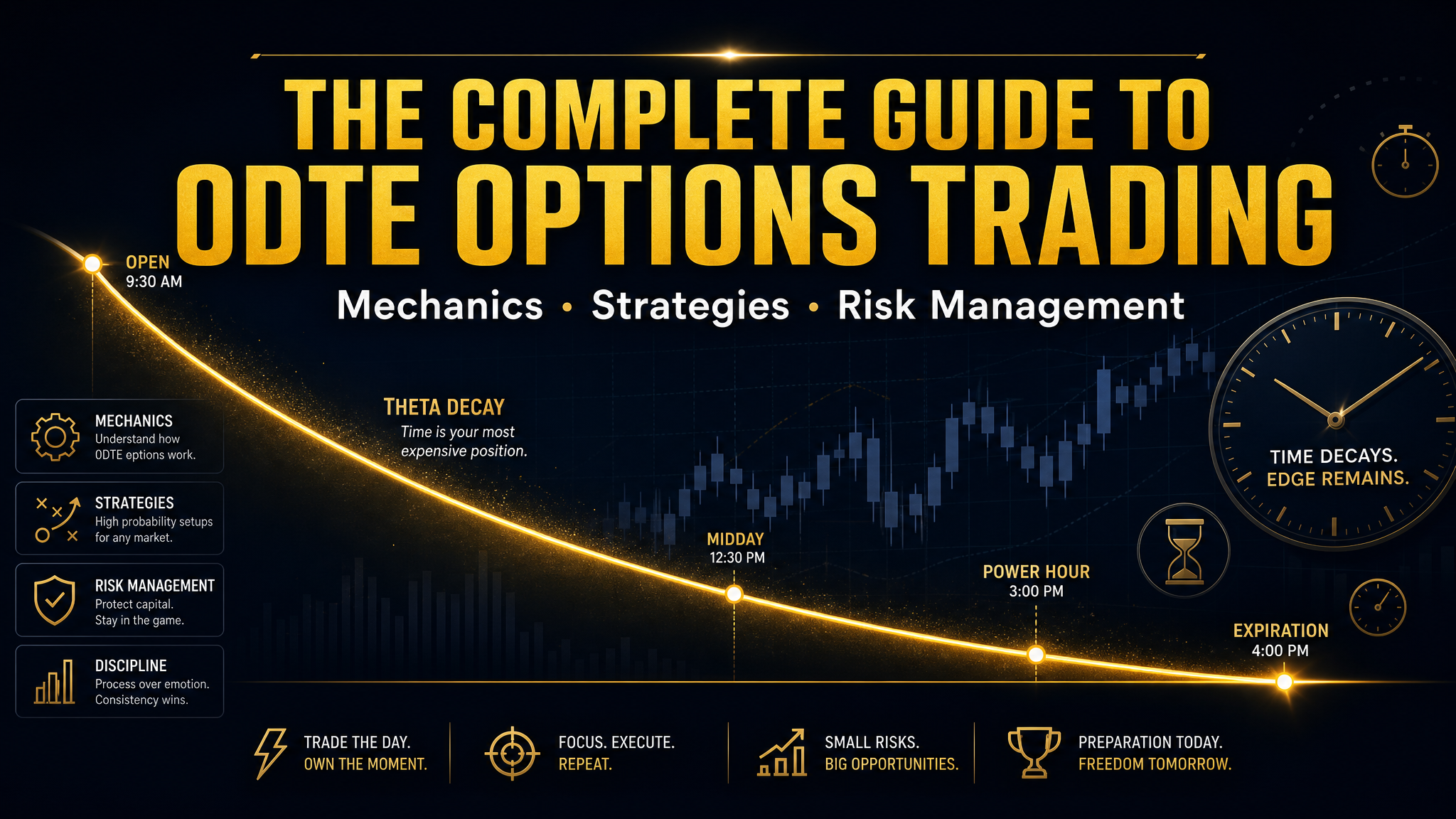

The Core Mechanics: Theta, Gamma & Time

To trade 0DTE options effectively, you need to understand two Greeks intimately: theta and gamma.

Theta (Θ) — Time Decay

Theta measures how much value an option loses per day from the passage of time. On a 0DTE option, this isn't gradual — it's exponential. The option loses value faster and faster as the close approaches, with the most violent decay occurring in the final 90 minutes.

For Debit Spread traders, timing is critical. Enter your Debit Spread during the optimal entry window when the move is developing — too early and theta works against you, too late and you overpay for a move that's already happened. SPXXL's theta decay curve shows you exactly when to strike.

Gamma (Γ) — The Accelerator

Gamma measures how fast delta changes for a $1 move in the underlying. On 0DTE options, gamma is extremely high near the money. A small move can flip a position from profitable to losing in minutes.

This creates the fundamental tension of 0DTE trading: theta rewards you for time passing, but gamma punishes you if the market moves. The best traders choose structures and timing that maximize theta capture while minimizing gamma exposure.

SPX vs SPY for 0DTE — Which and Why

While both SPX and SPY track the S&P 500, SPX offers decisive structural advantages for 0DTE trading:

- Cash settlement — No assignment risk. No share delivery. Settle in cash at expiration.

- 60/40 tax treatment — Under Section 1256, SPX gains are taxed 60% long-term / 40% short-term regardless of holding period.

- European exercise — Cannot be exercised early. No surprise assignments.

- No PDT rule — Index options are exempt from the Pattern Day Trader restriction.

- Deepest liquidity — SPX 0DTE volume exceeds all other index and ETF 0DTE combined.

📖 Deep dive: Why SPX Over SPY for 0DTE Options Trading →

The 5 Core 0DTE Strategies

Every 0DTE strategy falls into one of two camps: range-bound structures (Debit Condors/Butterflies) or directional structures (Bull Call/Bear Put Debit Spreads). Here are the five most common:

1. Debit Spreads (Bull Call / Bear Put)

Buy a closer-to-money option, sell a further-out option to reduce cost. Profit when the market moves in your chosen direction. This is the bread-and-butter 0DTE strategy — defined risk, defined reward, directional clarity.

2. Debit Condors

Combine a Bull Call Debit Spread and Bear Put Debit Spread. Profit when price stays within a range. Ideal for balanced, low-volatility sessions where the market consolidates around VWAP.

3. Debit Butterflies

A more aggressive version of the Debit Condor with strikes centered on the current price. Higher max profit but narrower profit zone. Best used when you have high confidence in a specific close zone.

4. Debit Spreads

Buy a closer-to-money option, sell a further-out option. A directional bet with limited risk. Used when session classification suggests a trending day with a clear directional bias.

5. Naked Long Puts/Calls

Pure directional speculation with unlimited upside but rapid time decay working against you. High risk/reward. Only appropriate when strong catalysts (FOMC, CPI) create outsized directional opportunities.

Risk Management — The Non-Negotiable Rules

0DTE trading without strict risk management is gambling. These rules separate professionals from speculators:

- Maximum 2-5% of portfolio per trade. No single 0DTE position should threaten your account.

- Use defined-risk structures. Debit Spreads, Debit Condors, Butterflies — always know your max loss before entry.

- Set mechanical exit rules. Close at 50-75% of max profit. Cut losses at 100% of debit paid. No discretionary holds.

- Avoid event days without adjustment. FOMC, CPI, and NFP days have different volatility profiles. Widen strikes or reduce size.

- Track every trade. Win rate, average P&L, drawdowns. You can't improve what you don't measure.

Session Classification: Reading the Market First

The single most impactful improvement a 0DTE trader can make is learning to classify the session type before choosing a structure. The market produces approximately six repeating session archetypes:

- Balanced Day — Mean-reverting, range-bound. Best for Debit Condors and Debit Butterflies.

- Trend Day — Directional move with conviction. Best for Debit Spreads in the direction of the trend.

- Expansion Day — Wide range, high volatility. Dangerous for range-bound structures. Consider sitting out or going directional.

- Volatility Compression — Narrow range, coiling volatility. Set up for a breakout. Reduce size.

- Short Covering Rally — Violent upside move as shorts cover. Fast and often fades.

- Liquidity Sweep — Price probes beyond support/resistance to trigger stops before reversing.

Each archetype has different win rates for different structures. Trading a range-bound structure on a Trend Day is a recipe for maximum loss. Trading Directional Spreads on a Balanced Day wastes premium.

The Optimal Trading Window

Not all hours of the 0DTE session are created equal. The decay curve and risk profile shift dramatically throughout the day:

- 9:30-10:00 (IB Formation) — The initial balance range is establishing. High gamma, low theta. Most professionals wait.

- 10:00-14:00 (Core Theta) — The sweet spot. IB is established, theta decay is accelerating, and the session type is becoming clear. This is when most premium sellers enter.

- 14:00-15:00 (Power Hour) — Institutional repositioning creates volatility. Theta accelerates but gamma risk increases. Manage existing positions; avoid new entries.

- 15:00-16:15 (Terminal) — Maximum theta decay but also maximum gamma risk. A 10-point SPX move here can flip any position. This is where beginners get destroyed.

📖 Deep dive: Best Time of Day to Trade 0DTE Options →

Tools and Technology for 0DTE

Successful 0DTE trading requires more than a broker and a chart. The speed and complexity of same-day expiration demand specialized tools:

- Real-time Greeks — Delta, gamma, theta updating continuously. Not delayed, not estimated — real-time.

- Gamma Exposure (GEX) data — Understanding dealer positioning reveals structural support, resistance, and the gamma flip level.

- Session classification — Quantitative identification of the current session archetype, replacing subjective chart reading.

- Theta decay curves — Visual representation of theoretical vs realized decay to identify when premium selling is most efficient.

- Excursion analysis — Historical maximum favorable/adverse excursion data for structure sizing and strike selection.

⚡ SPXXL provides all of this in a single dashboard — session classification, theta decay analysis, gamma exposure tracking, and structure recommendations. Try it FREE — 5 live sessions on us →

Building Your 0DTE Playbook

A playbook turns strategy into process. Here's a framework for building yours:

- Pre-market check — Review overnight futures, VIX level, GEX positioning, and any scheduled macro events.

- Session classification — Wait for the initial balance to form (first 30 min), then classify the session type.

- Structure selection — Match your strategy to the session archetype. Balanced Day = Debit Butterfly. Trend Day = Debit Spread with the trend. Expansion Day = reduce size or sit out.

- Entry — Define your entry criteria: time window, delta of long strike, debit paid, risk/reward ratio.

- Management — Set mechanical exits: close at 50% profit, close at 2x loss, close by 3:30 PM regardless.

- Review — Grade the session. Was your classification correct? Was the structure optimal? What would you change?